Most people evaluate debt as if income were guaranteed.

In reality, your income is your riskiest asset.

Debt is not dangerous in isolation.

Debt becomes dangerous when it collides with human capital risk.

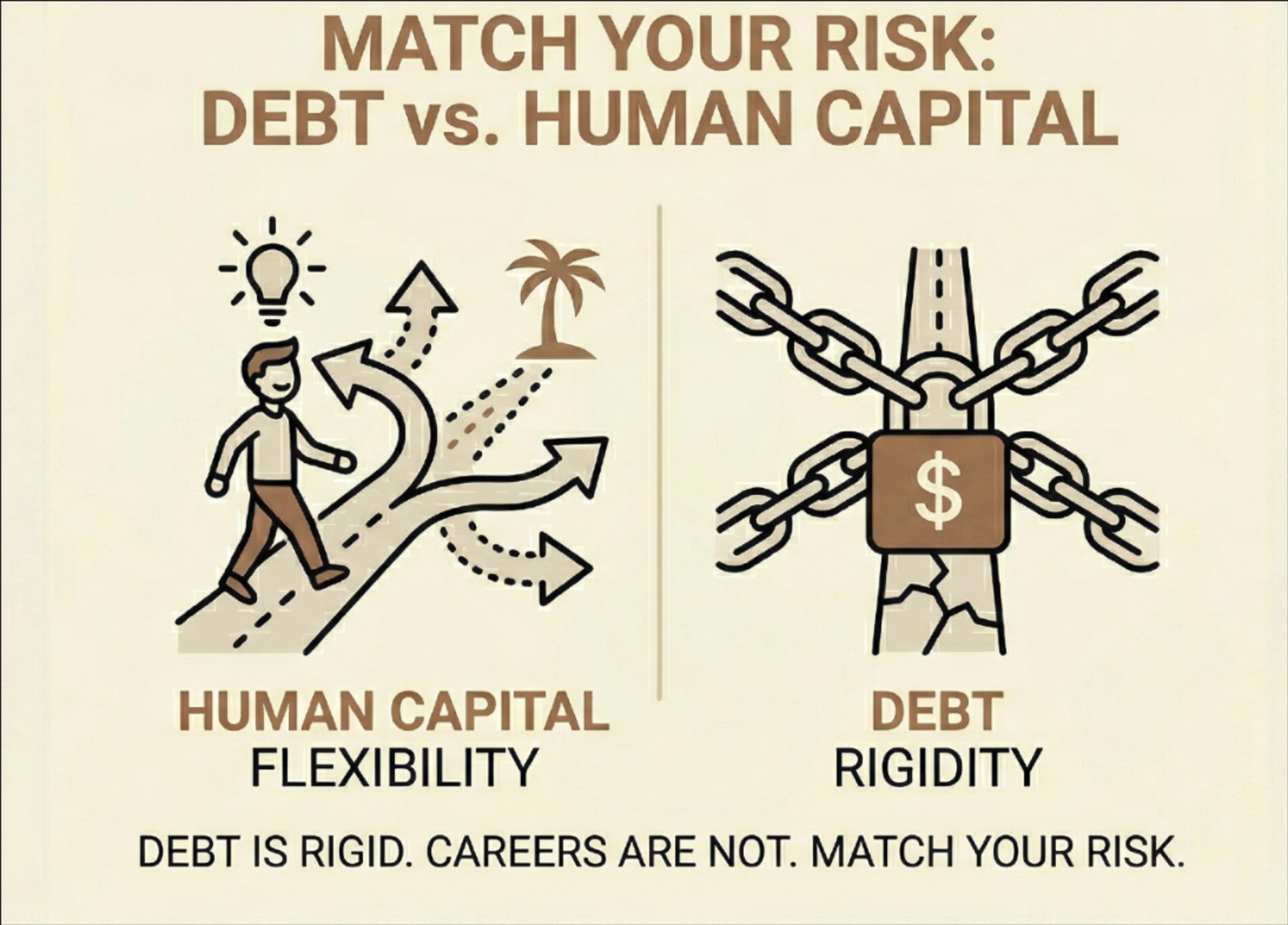

Human Capital: Your Largest, Least Diversified Asset

Human capital is the present value of your future earnings.

For most people, it represents:

70–90% of total lifetime wealth

A single income stream

Exposed to industry, geography, health, and timing risk

Unlike financial assets, human capital:

Cannot be rebalanced

Cannot be sold partially

Cannot be hedged easily

And yet, debt assumes it will behave smoothly.

Debt Assumes Stability Where None Exists

Debt contracts are rigid.

Human capital is not.

Debt implicitly assumes:

Continuous employability

Stable wages

Predictable career progression

But real careers look very different:

Non-linear paths

Voluntary and involuntary breaks

Sector-specific shocks

Skill obsolescence

Debt is priced as if income volatility were rare.

For individuals, it isn’t.

The Correlation Problem No One Talks About

The most underestimated risk is correlation between income and debt stress.

Income often drops when:

The economy slows

Markets decline

Credit conditions tighten

Exactly when:

Debt refinancing becomes harder

Asset values fall

Liquidity is most valuable

This is not bad luck.

It’s structural correlation.

Debt concentrates risk at the worst possible time.

Debt Turns Career Risk Into Financial Risk

Career risk is usually manageable:

You can switch roles

Change industries

Accept temporary income reductions

Debt removes that flexibility.

With debt:

Career experimentation becomes costly

Skill-building detours feel dangerous

Short-term income dominates long-term value

Debt pushes people to:

Stay in suboptimal jobs

Avoid entrepreneurial paths

Prioritize stability over growth

It quietly reshapes careers — often downward.

Why “Safe Jobs” Still Carry Debt Risk

Even traditionally stable professions face human capital risk:

Technological disruption

Regulatory changes

Health limitations

Burnout

Debt magnifies these risks by:

Increasing required income floors

Reducing tolerance for transitions

Penalizing recovery time

The problem isn’t job security.

It’s income rigidity paired with obligation rigidity.

The Asymmetry Between Debt and Human Capital

Human capital risk is asymmetric:

Downside is immediate

Recovery is slow

Timing matters more than averages

Debt ignores this asymmetry.

A short income disruption can:

Trigger forced asset sales

Destroy compounding

Permanently alter financial trajectories

This is why debt is often survivable — but career-damaging.

A More Honest Way to Evaluate Debt

Instead of asking:

“Can I afford the payments today?”

Ask:

“What happens if my income drops 30% for 12 months?”

If the answer involves:

Liquidating long-term assets

Abandoning strategic goals

Taking any job at any cost

Then the debt is misaligned with your human capital risk.

Matching Debt to Human Capital Quality

Debt is safest when human capital is:

Highly in-demand

Transferable across industries

Geographically flexible

Not tied to economic cycles

Debt is dangerous when human capital is:

Specialized

Cyclical

Location-dependent

Physically or mentally demanding

This is not about intelligence or effort.

It’s about risk matching.

Human Capital First, Balance Sheet Second

Most people optimize their balance sheet while ignoring their income statement.

This is backwards.

Before taking on debt, the priority should be:

Strengthening employability

Increasing income flexibility

Building optionality

Debt should come after resilience, not before it.

Final Thought

Debt assumes the future will cooperate.

Human capital proves it rarely does.

The real danger of debt is not default —

it’s locking your financial life to a single, fragile income trajectory.

When debt and human capital risk are misaligned,

even small shocks can cause permanent damage.

Design debt around uncertainty — not optimism.