Why traditional active funds are legally safe, but mathematically dangerous for your financial independence.

When you first decide to invest, the easiest route is often walking into your local bank or speaking with a financial advisor. In 99% of these conversations, you will be pitched a Mutual Fund (or Fondo Comune d’Investimento if you are based in Europe).

On the surface, mutual funds sound great. They pool money from thousands of investors to buy a diversified basket of stocks or bonds, all managed by a team of “experts” in suits. But if you are on the path to FIRE (Financial Independence, Retire Early), you need to look under the hood.

While mutual funds are built on a solid legal framework designed to protect your capital from fraud, their fee structures are often designed to slowly drain your long-term returns. Here is the reality of how mutual funds work, and why they often fall short for the serious wealth builder.

The Good: Structural Safety

Let’s start with the positive. From a legal standpoint, mutual funds are incredibly safe vehicles.

In Europe, the legal framework dictates a strict separation between the Management Company (the entity picking the stocks) and the Fund’s Assets (your money). The fund is constituted as an autonomous asset pool.

Why does this matter? Because if the management company goes bankrupt, your money is completely untouched. Your assets belong to you and the other investors, not to the company managing them. Furthermore, the management company is legally bound to act in the exclusive interest of the participants.

Structurally, they are sound. The problem isn’t the legal setup; it’s the cost of the management

.

The Bad: The Tyranny of Compounding Costs

John Bogle, the legendary founder of Vanguard, famously said: “The miracle of compounding returns is overwhelmed by the tyranny of compounding costs.” Mutual funds are predominantly actively managed. This means a team of analysts is constantly buying and selling assets, trying to “beat the market.” This activity is expensive, and the investor foots the bill. Here is how your returns are drained:

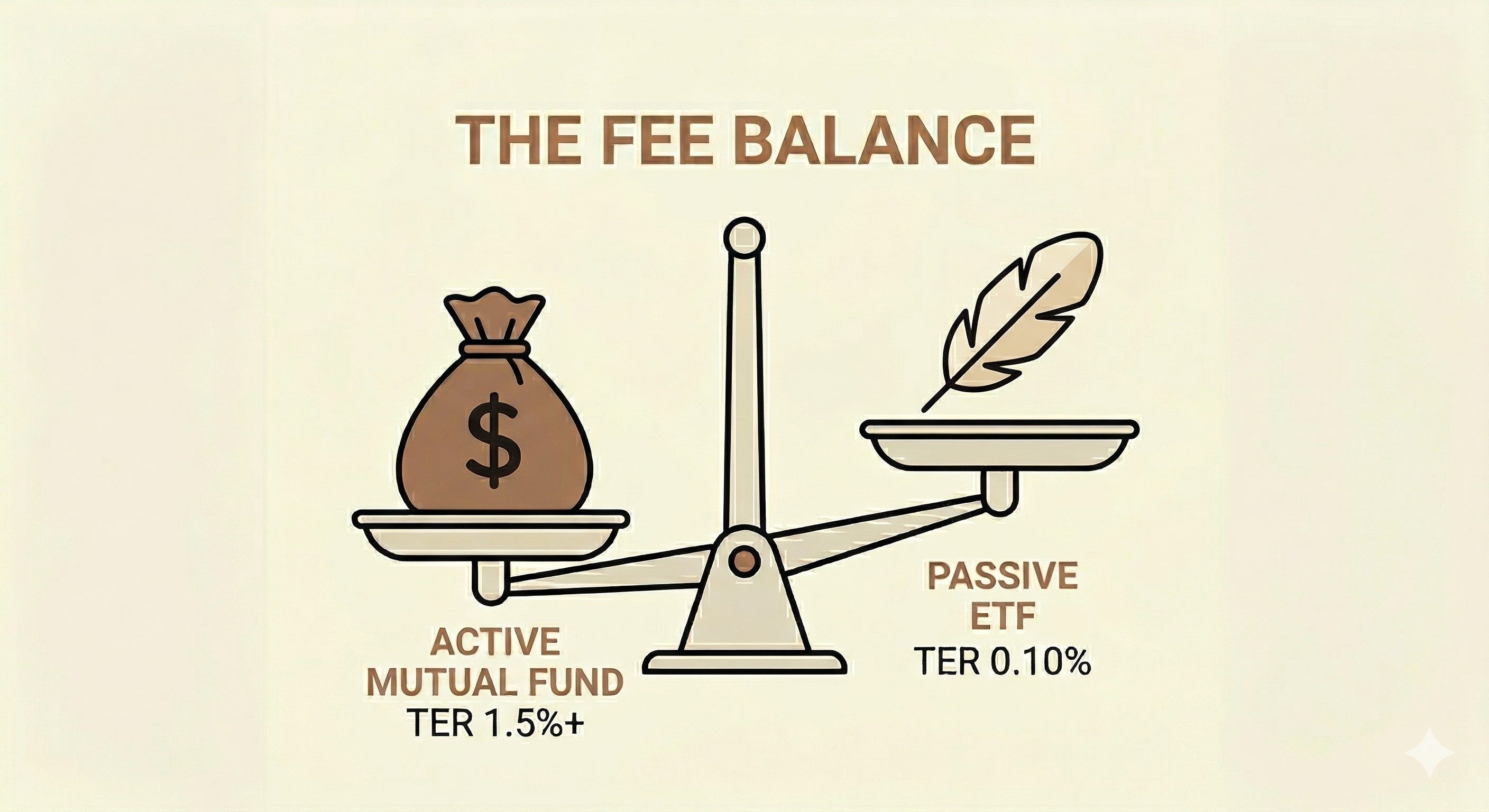

1. The TER (Total Expense Ratio)

Every fund has an annual management fee. For active mutual funds, a TER of 1.5% to 2.5% is standard. If the market returns 7% in a given year, a 2% TER leaves you with just 5%. Over a 20-year investing horizon, that 2% annual drag can easily eat up over 30% of your total potential wealth.

2. Entry and Exit Fees

Many traditional mutual funds charge a “subscription fee” when you buy in, or a “redemption fee” when you sell. Paying 1% or 2% just for the privilege of handing over your money puts you in the red before your investment has even seen a single day of market action.

3. Performance Fees (The Ultimate Trap)

Some active funds charge a performance fee on top of the TER. If the fund manager beats their benchmark, they take a percentage of your profits (often 10% to 20%).

Notice the asymmetry here? Heads they win, tails you lose. If the manager does exceptionally well, they take a cut of your upside. If they perform terribly, they don’t refund you; you simply absorb the loss (and still pay the standard TER).

Mutual Funds vs. ETFs: The Passive Revolution

Active mutual fund managers have a very difficult job. To justify their high fees, they don’t just have to beat the market—they have to beat the market by a margin large enough to cover their costs.

Statistically, over a 10 to 15-year period, more than 85% of active mutual funds fail to beat their benchmark indices.

This is why the core of the FIRE philosophy relies on Exchange-Traded Funds (ETFs).

The Goal: ETFs don’t try to beat the market; they simply track it (passive management).

The Cost: Because there is no team of highly paid analysts trying to guess the future, the TER of a broad-market ETF is often between 0.05% and 0.20%.

The Result: By eliminating entry fees, exit fees, performance fees, and high management costs, the ETF investor captures almost 100% of the market’s return.

Final Thought

Mutual funds played an important role in the history of democratizing finance, allowing retail investors to easily access diversified portfolios. However, the financial industry has evolved.

When you buy a traditional, actively managed mutual fund, you are effectively hiring someone to play a guessing game with your money, and agreeing to pay them whether they win or lose. For the modern investor focused on long-term wealth, the formula is clear: minimize costs, buy the whole haystack through broad index ETFs, and let compounding do the heavy lifting.