When it comes to building long-term wealth, many investors are familiar with the comforting rhythm of Dollar Cost Averaging (DCA)—investing a fixed amount at regular intervals, regardless of market conditions. It’s simple, systematic, and, frankly, better than procrastinating on the sidelines. But for those willing to add a layer of discipline, flexibility, and—yes—a little math to their financial routine, Value Averaging (VA) might be the game-changer they’ve been overlooking.

The Fundamental Difference: DCA vs. VA

At first glance, both DCA and VA belong to the family of Capital Accumulation Plans (CAPs). Both aim to help investors grow their portfolio while reducing the emotional rollercoaster tied to market fluctuations. But that’s where the similarities end.

DCA commits you to a fixed investment—say €100 every month—buying more shares when prices are low and fewer when they’re high. Over time, it smooths out your average purchase price, lowering the risk of buying in at market peaks.

VA, however, flips the script. Instead of contributing a constant amount, you target a constant growth in portfolio value. If your portfolio has underperformed this month, you invest more to get back on track. If it has surged ahead, you scale back your contribution—or even withdraw capital. The objective? Systematically “buy low, sell high” without relying on emotions or predictions.

The Beauty of Methodical Flexibility

Introduced by Michael E. Edleson in 1993, VA was designed to appeal to rational, goal-oriented investors. It recognizes a truth that market timing rarely admits: predicting price movements is a fool’s errand, but controlling your own contributions is within reach.

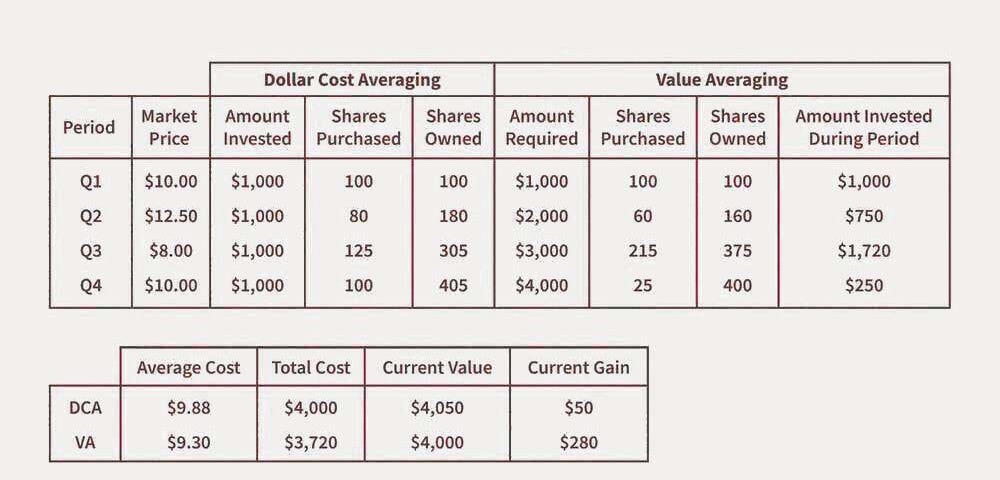

Consider this practical example:

Month 1: You invest €1000, buying 100 shares at €10 each.

Month 2: The price jumps to €12.50. A DCA plan buys 80 shares, sticking to the €1000 rhythm. A VA plan? It only contributes €750 to realign your portfolio to the pre-set value target.

The brilliance lies in how VA dynamically adjusts to market performance. It increases contributions when prices fall, ensuring you’re capitalizing on undervalued assets, and eases off when prices rise, locking in gains without emotional interference.

But Let’s Be Honest: VA Isn’t Perfect

With sophistication comes complexity, and VA is no exception. Critics are quick to point out its downsides:

Manual Execution: Most platforms cater to DCA; VA requires you to track, calculate, and execute irregular contributions. It demands more attention and discipline than many investors are used to.

Variable Payments: Some months might require unexpectedly large investments, particularly after market dips—a challenge for those with tight cash flow or fixed investment budgets.

Performance Measurement Nuances: Residual liquidity, excess cash sitting idle, can distort returns and complicate portfolio evaluation. Simon Hayley’s research highlights this subtle yet crucial limitation.

Volatility Dependency: VA shines with moderately volatile assets, but excessive swings (think crypto or small-cap equities) could trigger risky overexposure. Conversely, applying VA to low-volatility assets dilutes its advantages.

Yet, as with most investment tools, context and execution matter. Investors equipped with proper risk management, diversification, and patience can sidestep many of VA’s pitfalls.

My Perspective: A Pragmatic, Balanced View

In my opinion, VA isn’t a “magic formula,” but it’s an underutilized strategy with real merit—especially for methodical investors who value structure and have liquidity to deploy strategically. It elegantly embodies the “buy low, sell high” mantra without requiring speculative guesswork. But, and this is key, it demands preparation: flexibility in contributions, a willingness to monitor performance, and access to liquid reserves.

What fascinates me about VA is its psychological advantage. By design, it curbs the temptation to chase market highs or panic during downturns. Much like DCA, it introduces automation, but with an intelligent, responsive twist. For those who embrace this discipline, VA can mitigate emotional decision-making and cultivate stronger, more resilient portfolios.